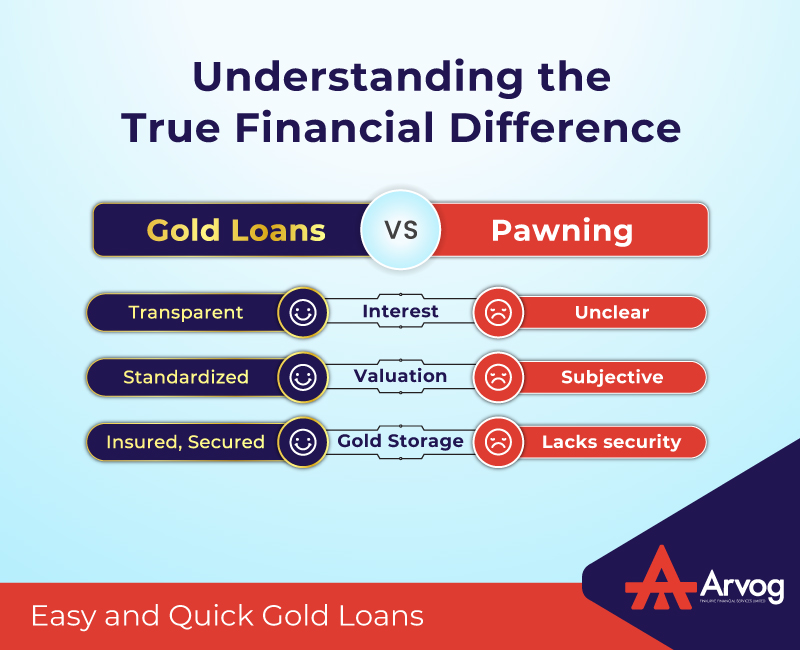

In today’s information era, one of the most important factors in achieving business success is learning how to assess and get value from our company’s digital insights. Financial institutions have been considering the borrower’s income and employment stability before approving a loan.

And now, with the help of advanced data analytics technologies, it is feasible to make sense of this data and take action in ways that were previously unimaginable.

The Influence of Data Analytics :-

Analytics, in its historical context, can be defined as “the study of analysis.” To gain business insights and provide individualized responses to customers, “data analytics” has emerged as a more practical and up-to-date term. The business has been using these analytics since at least the 19th century when Frederick Winslow Taylor introduced time management techniques. Henry Ford also monitored the production rate of his assembly lines. With the rise of the personal computer as a tool for making decisions, the field of analytics gained prominence in the late 1960s. Then, to streamline, quicken, and even automate the analytics process, companies have been using electronic technologies including, databases with relational structure, data storage facilities, ML (machine learning) algorithms, internet-based search solutions, charts and graphs, and more since at least the 1970s.

When it comes to making important strategic and operational lending decisions, businesses depend on the insights gleaned from analytics processes and technologies.

Role of Data Analytics in Lending:-

Credit risk assessment may be challenging and inaccurate for several reasons, including a lack of appropriate data, poor data processing by credit risk assessors, and a time-consuming review procedure.

These risks can be reduced and accuracy improved by using Big Data Analytics. Let’s examine the advantages it offers.

1. Collecting Information and Analyzing :-

Financial institutions may streamline their consumer segmentation efforts with the help of a data analytics platform. Lenders may use this data to learn about their potential customers’ financial standing, spending habits, and credit preferences. There is a significant opportunity for cost savings for businesses that are open to exploring new and more effective approaches to bank lending decisions.

2. Predictive Model Construction :-

Predictive analytics is rapidly becoming the most popular subset of data science. This feature is used in business to spot patterns and establish links between events.

Mortgage companies, for instance, may improve customer retention and cut down the losses by looking at things like consumer buying habits, social media profiles, and employment records.

3. Quantitative Risk Analysis and Credit Scoring :-

Creditworthiness assessment has become increasingly difficult in recent years, as noted by several professionals in the field. Young adults don’t often have a lengthy credit history since they don’t use credit cards or buy cars. So, mortgage companies are trying out new methods of vetting applicants. The use of big data and analytics on such data may help bridge that gap.

4. Identification and Prevention of Fraud :-

Data analysis is also used to uncover fraud. A thorough investigation of clients’ finances, purchasing patterns, and credit information, businesses might reveal anything suspicious. In addition to official documentation, an individuals’ financial information may be used to verify their identity. Since this is the case, authenticating it requires data analysis.

5. Timely Decision Making :-

Decision-making assistance from machine learning models is available for all bank-defined workflows. It is possible to automate every step of the loan process, from client segmentation through interest rate approval to repayment tracking. This has the potential to drastically cut down on the time and money needed for processing loans and making lending decisions internally.

After the 2008 global financial crisis, regulatory and statutory credit risk management requirements tightened, making credit risk assessment and lending decisions more challenging. The growth of fintech startups with big data analytics has outpaced most nations’ legislative revisions. Fintech businesses can now quickly evaluate loan applications while complying with legislation.

Emerging Trends :-

Today’s leading business intelligence (BI) tools increasingly use AI and machine learning (ML) to better serve corporate customers. Fortune Business Insights predicts that by 2030, the business intelligence industry will be worth $54.27 billion, a $27 billion rise from 2022.

More and more information is being generated every day, making it essential for businesses to adopt data-driven strategies. However, not every company has the resources of the greatest technology firms to quickly gather, store, and analyze data to make quick lending decisions.

DaaS, or “Data as a Service,” could be a solution to this problem. Data as service providers usually provide subscription-based data collecting, storage, and analysis services. Instead of processing and storing data locally, it processes and provides it through cloud computing, which is sent to end users via the Internet.

Most companies would benefit from investing in a data hub or data pool equipped with the appropriate tools due to an abundance of data sources and the sheer amount of data they generate. And that is particularly true in the lending decisions made in the financial industry. The ability to adapt quickly to new circumstances and use data analytics in the appropriate business processes will define market leaders.

Who We Are:-

Arvog is a new-age, AI/ML-powered, customer-centric finance company that makes digital lending quick, efficient, and easy. We focus on digital personal loans and digital gold loans.

{kind=link}