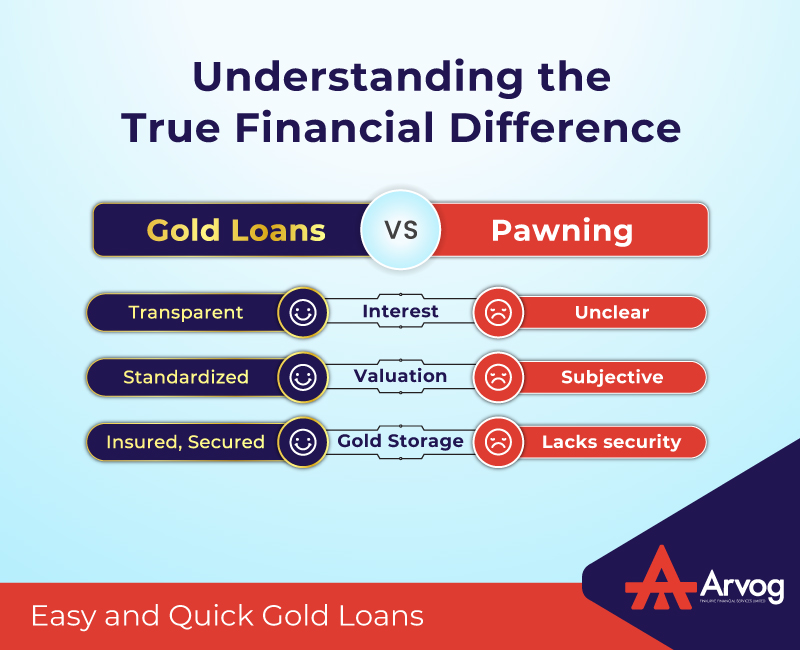

The gold loan stands out as the most straightforward and convenient credit option, particularly in the context of a typical Indian household. Gold, regarded as an invaluable asset acquired during festive and family occasions like births or marriages, serves as readily available collateral for unforeseen or planned expenses. While lenders may boast about offering the best gold loan deals, the crucial factors are gold valuation and the loan-to-value (LTV) ratio. The LTV ratio determines the maximum amount a borrower can secure through a secured loan based on the current market value of the pledged asset, making it a key factor in obtaining a gold loan.

Although LTV is a predetermined value for many lenders, certain ones may determine the actual ratio based on the borrower’s application. This is due to the LTV ratio representing the loan amount borrowers can receive for the market value of the pledged gold. For instance, a lender might provide a 65% loan-to-value ratio on a gold loan. In this case, if the pledged gold jewelry is valued at Rs. 2 Lakhs, the borrower can receive a maximum loan amount of Rs. 1.3 Lakhs.

Here are some important pointers related to gold valuation and loan-to-value:

Precious stones and making charges paid: It’s crucial to bear in mind that the assessment of gold (collateral) isn’t reliant on the price paid for the gold items. When purchasing gold jewelry, the buying price typically encompasses making charges and the worth of any precious or semi-precious stones. The loan-to-value (LTV) ratio, however, is determined solely based on the actual weight of the gold. The making charges and the stone weights are not factored into the calculation of the gold’s value. Nevertheless, the applicable gold rate used for the calculation must align with the current market rate or the average rate over the preceding days, and this can vary among different lenders.

Valuation at the current rate: Calculating the value of gold at the current market rate provides borrowers with a distinct advantage. This is because gold is an appreciating asset, and typically, individuals acquire gold at lower rates than the prevailing ones. Consequently, the value of gold increases over time, leading to a higher loan amount. For instance, a gold ornament purchased a few years ago with 20 grams of gold at Rs. 3,000/- per gram would have initially been valued at Rs. 60,000/-. Now, with a current gold loan rate of Rs. 5,500/- per gram, the gold’s value is considered to be approximately Rs.1,10,000/- for loan calculation purposes.

Loan-to-Value Ratio: The loan-to-value ratio, governed by the RBI guidelines, undergoes periodic revisions. A higher LTV sanctioned by RBI for gold loans implies that borrowers can access a greater loan amount for the same gold value compared to previous limits. For instance, with a gold valuation of Rs. 2 lakhs and a 75% LTV, the borrower can secure a loan of up to Rs. 1.50 lakhs whereas at a 65% LTV, the loan value is limited to Rs. 1.30 lakhs only.

Higher LTV may not always be good: At first glance, a higher Loan-to-Value (LTV) may appear favorable for borrowers. Nonetheless, loans featuring elevated loan-to-value ratios typically entail increased interest rates, posing added risk as borrowers become accountable for repaying a larger amount.

Arvog is a new-age, AI/ML-powered, customer-centric finance company that makes digital lending quick, efficient, and easy. We see worth in lending wings to people’s aspirations, hopes, and dreams. We believe purpose-driven credit can be a true-life enabler. Arvog is here to lend a helping hand, with affordable loans designed specifically for those who need them the most.

Arvog empowers NBFCs and fintechs with the tools and solutions they need to get fast access to credit, thus building more resilient and confident communities.