The RBI advisory released in May 2024 limited the cash disbursements to Rs. 20,000, promoting a shift to digital channels. This led to a minor increase in turnaround and the processing time of gold loans. Despite this, the Indian gold loan market reported a growth of 12% in June 2024 disbursements. The growth consistency can be attributed to the robust credit demand rising from emerging consumerism and the market resilience leading to an increase in gold prices.

The Reserve Bank of India (RBI) advised several gold-loan Non-Banking Financial Companies (NBFCs) to comply with the provisions of the Income Tax Act. The regulator directed to limit the cash disbursals of loans to Rs. 20,000. The directive mandates to digitally transfer the disbursals over Rs. 20,000 into the borrower’s account. Despite such norms, the demand for gold loans reported growth. This is driven by the working capital requirements of the fast-growing MSMEs, agri-sector, and other small businesses in rural and semi-urban areas.

Limit on Cash Disbursements

This directive stipulates that loans exceeding ₹20,000 cannot be disbursed in cash and must instead be processed through banking channels such as National Electronic Funds Transfer (NEFT), Real Time Gross Settlement (RTGS), or Unified Payments Interface (UPI). The NBFCs dominate the Indian gold loan market with over 61 percent market share, and the balance 31 percent is catered by the banks. Until May 2024, up to 95% of gold loans disbursed by NBFCs were given in cash to ensure quick service for borrowers. With the new directive in force, NBFCs have successfully shifted to digital channels with only a minor increase in processing time, allowing them to maintain their advantage over banks. This smooth transition was made possible by their existing infrastructure and technology, which were already equipped to handle online disbursements for larger loans, as well as efforts to educate borrowers on using digital methods.

Directives Implications

Undoubtedly the regulatory measures aim to tighten processes, eliminate the loopholes, ensure due-diligences for speedier recovery and improve the overall credit standards. However, it also adds to the compliances and operational costs to the gold loan provider.

Impact on Gold Loans

Despite this, the market for gold loans is expanding. And the demand for gold loans is also rising. The larger reasons for this demand are robust consumerism backed by equally strong economic growth and also the rising gold prices. The main growth drivers of gold loans are MSMEs, small traders, and farmers from rural and semi-urban areas across India. This consumer segment does not have much knowledge about other financial services and depends on traditional loan products, like gold loans, for their short-term capital requirements. Additionally, the increasing gold prices too provide apt cushioned loan-to-value (LTV) to the lender, and at the same time, the borrower gets better value for the gold.

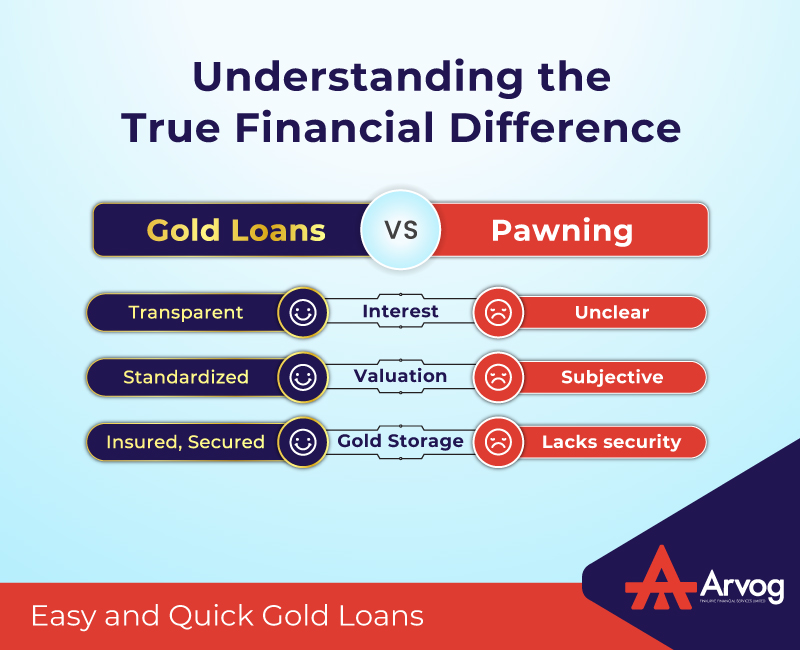

The other factors making a gold loan the first choice in need of finance are that it is hassle-free, requires the least documentation, has faster approval, and last but not least, the credit history of the borrower is not required for a gold loan.

Arvog is a new-age, AI/ML-powered, customer-centric finance company that makes digital lending quick, efficient, and easy. We see worth in in lending wings to people’s aspirations, hopes and dreams. We believe purpose-driven credit can be a true-life enabler. Arvog is here to lend a helping hand, with affordable loans designed specifically for those who need them the most.

Arvog empowers NBFCs and fintechs with the tools and solutions they need to get fast access to credit, thus building more resilient and confident communities.

Economic Times Industry Report:

The Hindu Business Line: