Cash flow is rarely uniform. For most Indian households, farmers, traders, and MSMEs, income and expenses move in cycles not straight lines. There are months of abundance and months of tight liquidity. School admissions, festive seasons, crop sowing, inventory stocking, tax payments, wedding months – each brings predictable yet temporary financial pressure.

The real challenge is not earning money. It is managing timing.

This is where gold loans emerge as a strategic short-term financial tool not just an emergency option, but a planned liquidity solution aligned with seasonal cash flow cycles.

Understanding Seasonal Cash Flow Cycles

Seasonal cash flow refers to periods when expenses peak before income is realized.

- Farmers: Investing Before Harvest

For farmers, expenses come first. Seeds, fertilizers, pesticides, irrigation, labour all require upfront capital. Revenue, however, arrives only after harvest and sale.

A chilli farmer, for instance, may need funds in June for sowing but receives income only in October or November. Without accessible short-term liquidity, he may miss optimal sowing windows – directly impacting yield.

In such cases, pledging gold jewellery for a short-term gold loan helps bridge that gap. Once harvest income arrives, the loan can be repaid comfortably.

Gold becomes working capital.

- MSMEs: Inventory and Working Capital Cycles

Small manufacturers, retailers, and traders often face similar timing mismatches.

Consider a garment retailer preparing for the festive season. Inventory must be stocked months in advance – payments to suppliers are immediate. Sales revenue, however, flows in gradually during the season.

Similarly, a small fabrication unit may receive payments 60–90 days after delivering goods. Meanwhile, salaries, electricity bills, and raw material purchases cannot wait.

In such scenarios, gold loans offer quick working capital without lengthy approval processes typical of traditional business loans.

- Households: Predictable but Pressured Months

Even salaried families face cyclical strain:

- School admissions and annual fees

- Insurance premium renewals

- Festival shopping

- Medical expenses

- Tax payments

These are predictable events — yet they create short-term liquidity crunches.

Instead of breaking long-term investments or swiping high-interest credit cards, many families use gold loans to temporarily unlock the value of idle jewellery.

Why Gold Loans Fit Seasonal Needs

The strategic advantage of gold loans lies in their structure. They are naturally suited for short-term funding.

Let’s explore the key features that make them ideal for managing seasonal cash flow.

Key Features of Short-Term Lending via Gold Loans

- Quick Processing and Disbursal

Seasonal needs are time-sensitive. A farmer cannot delay sowing. A retailer cannot miss stocking deadlines.

Gold loans are known for:

- Minimal documentation

- Fast valuation

- Same-day or near-instant disbursal

This speed ensures that opportunities are not lost due to funding delays.

- Short Tenure Options

Unlike long-term loans that stretch over years, gold loans are typically structured for shorter durations often 6 to 12 months.

This aligns perfectly with seasonal cycles:

- Crop cycle repayment after harvest

- Festive season inventory repayment after sales

- Annual expense repayment after bonus or business inflow

Borrowers use the loan precisely for the duration needed — not longer.

- Flexible Repayment Structures

Another advantage is repayment flexibility. Depending on the lender, borrowers may choose:

- Bullet repayment (pay interest during tenure, principal at end)

- Monthly interest servicing

- EMI options

- Part-prepayment without heavy penalties

For example, a trader expecting a lump sum payment in three months may prefer a bullet repayment model. A farmer anticipating phased crop sale may opt for periodic interest servicing.

Flexibility reduces stress.

- No Income Proof Complexity

Seasonal earners often struggle to produce conventional income documentation.

Farmers may not have formal salary slips. Small traders may operate with variable monthly revenues.

Since gold loans are collateral-backed, eligibility depends primarily on the value of pledged gold — not rigid income criteria. This makes them highly accessible for rural and semi-urban borrowers.

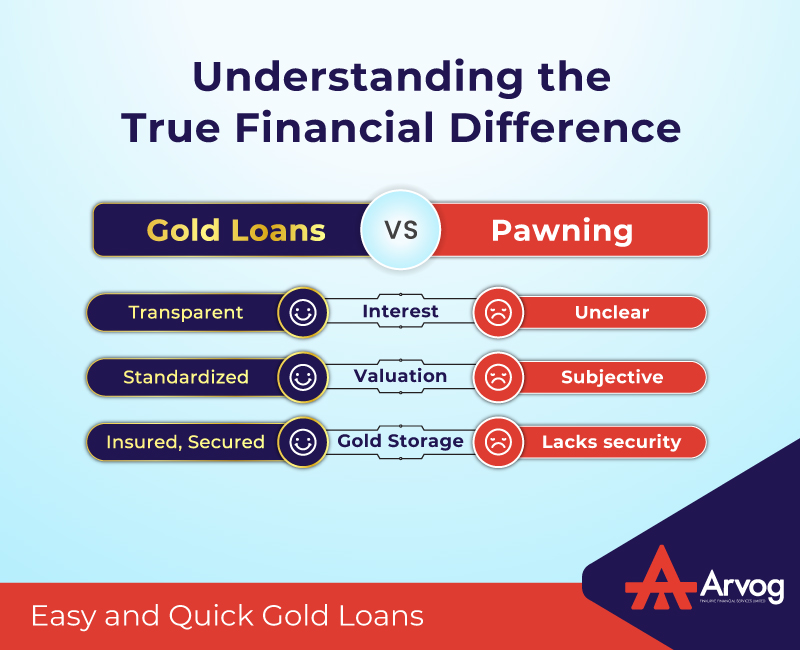

- Transparent Valuation Linked to Market Prices

Loan eligibility is based on prevailing gold rates and purity testing. Borrowers clearly understand:

- Gold weight assessed

- Purity level

- Applicable gold rate

- Eligible loan amount

This transparency ensures that borrowers unlock maximum value during periods when gold prices are favourable.

- Lower Processing Complexity Compared to Business Loans

Traditional working capital loans may require:

- Financial statements

- GST returns

- Income tax filings

- Collateral documentation

- Long approval timelines

For a small MSME facing an urgent requirement, this process may be too slow.

Gold loans, on the other hand, provide liquidity without extensive paperwork — making them practical for short-term bridging.

Strategic Use vs. Emergency Use

Many people view gold loans purely as an emergency option. However, when aligned with predictable seasonal cycles, they become strategic tools.

For example:

- A dairy farmer may regularly pledge gold during lean milk production months and release it during peak sale months.

- A cracker wholesaler may use gold loans annually before Diwali stocking.

- A tuition centre owner may bridge cash flow before academic year admissions peak.

In such cases, gold loans are not reactive — they are planned components of financial management.

Preserving Long-Term Investments

Breaking fixed deposits or redeeming long-term investments prematurely can lead to:

- Loss of accumulated returns

- Penalties

- Tax implications

Using a short-term gold loan instead allows individuals to maintain their long-term financial strategy while addressing temporary liquidity needs.

The jewellery remains safe in secure storage and can be reclaimed upon repayment.

Managing Risk Responsibly

While gold loans are effective tools, they should be used responsibly:

- Borrow only what is needed

- Align tenure with expected income cycle

- Understand interest structure clearly

- Plan repayment before pledging

When used with foresight, gold loans help smooth financial cycles rather than complicate them.

Gold as a Financial Buffer

In many Indian households, gold serves multiple roles — cultural, emotional, and financial.

During seasonal fluctuations, it becomes a buffer asset. It transforms from ornament to opportunity.

Instead of remaining idle in lockers, it can temporarily support:

- Crop production

- Business expansion

- Inventory stocking

- Education fees

- Medical needs

And once the cash flow stabilizes, it returns home.

Conclusion: Timing Is Everything

Financial success is not just about how much you earn — it is about managing when you earn and when you spend.

Seasonal cash flow cycles are natural across agriculture, trade, small business, and households. The key is to bridge the timing gap efficiently.

Gold loans offer:

- Speed

- Simplicity

- Flexibility

- Accessibility

- Short-term alignment

They are not merely loans — they are liquidity solutions designed for cyclical economies.

When used strategically, gold loans turn seasonal pressure into manageable planning — ensuring that opportunity is never lost simply because cash flow arrived a little later than expenses.