Gold prices directly influence gold loans. An upward movement in gold prices adds momentum to gold loans as borrowers unlock the potential of their invested gold for liquidity. Rising gold prices also make lenders’ portfolios safer, as they can maintain a good loan-to-value ratio. Read further to learn how fluctuating gold prices impact gold loans.

Gold loans have increasingly become a popular and smart choice for meeting unexpected financial needs. Many borrowers focus primarily on the interest rates, processing fees, and other charges associated with gold loans. However, some prudent individuals also strategize to minimize their gold loan costs. Despite this, a crucial aspect that is often overlooked is the impact of gold prices on gold loans. The fluctuation in gold prices significantly affects both the interest rates of gold loans and their overall demand.

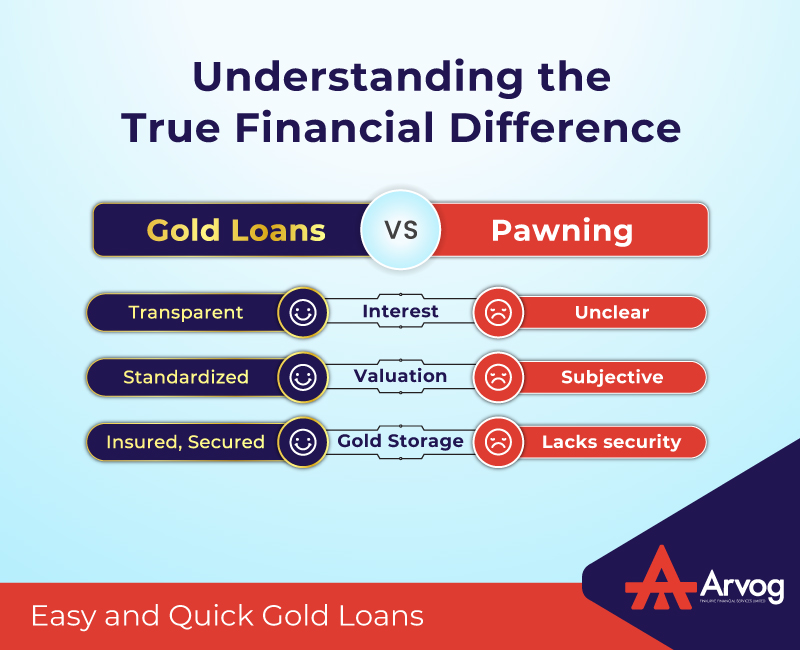

A fundamental principle of gold loans is that the borrower must pledge their gold jewellery as collateral against the loan amount. Once the loan is fully repaid, the lender returns the pledged gold jewellery to the borrower. Throughout the loan tenure, the pledged gold is securely stored, as detailed in a formal agreement adhering to the prevailing norms.

Gold Loan Loan-to-Value (LTV)

One important concept in gold loans is the loan-to-value (LTV) ratio. The LTV ratio determines the maximum loan amount that a lender can approve based on the total value of the gold pledged by the borrower. The Reserve Bank of India (RBI) has set a cap on the LTV ratio for gold loans at 75% for both non-banking financial institutions (NBFCs) and banks. For example, if a borrower pledges gold worth Rs. 1 lakh, the maximum loan amount they can receive is Rs. 75,000.

LTV and Gold Prices

The relationship between LTV and gold prices is critical. If we consider the same scenario and assume that the price of gold increases by 10%, the value of the pledged gold would rise from Rs. 1 lakh to Rs. 1.10 lakh. Consequently, with the increased gold price, the LTV of 75% would translate to a higher loan amount of Rs. 82,500. Thus, borrowers could secure a larger loan amount when gold prices increase.

Conversely, if gold prices decline, the loan value decreases as well. For instance, if the value of the pledged gold drops from Rs. 1 lakh to Rs. 90,000, the maximum loan amount the borrower could obtain would be Rs. 67,500. This inverse relationship underscores the importance of gold prices in determining the loan value.

In summary, gold loans offer a viable solution for unplanned financial needs, with several factors influencing their cost and value. Interest rates, processing fees, and other charges are primary considerations for borrowers. However, understanding the impact of gold prices on gold loans is equally essential. The LTV ratio, capped at 75% by the RBI, directly correlates with the value of the pledged gold. As gold prices rise, borrowers can secure higher loan amounts, while a decrease in gold prices results in lower loan values. By keeping an eye on gold price trends, borrowers can make more informed decisions and potentially maximize their loan benefits.