When you need quick funds, pledging gold is often the fastest and most accessible option. In India, gold is more than jewellery it’s a store of wealth, a financial safety net, and in many cases, the most reliable collateral during urgent times. However, many borrowers still confuse organised gold loans from regulated lenders with traditional pawning from local moneylenders. While both involve pledging gold in exchange for cash, the similarities largely end there.

Understanding the difference can help you protect not just your jewellery, but also your financial wellbeing. Let’s break it down across five critical factors.

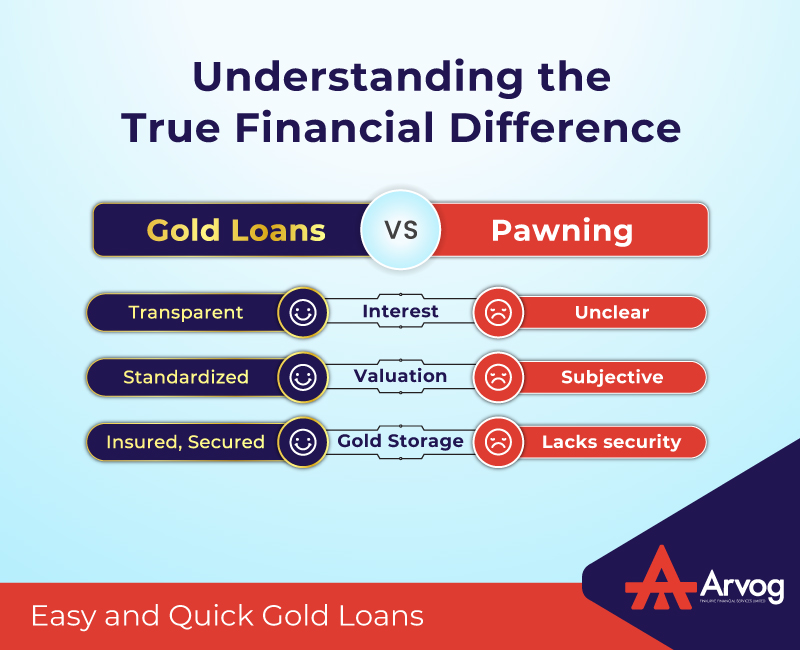

- Interest Structures: Transparent vs. Arbitrary

One of the most important differences lies in how interest is calculated and disclosed.

In organised gold loans offered by regulated NBFCs, lenders like Arvog Gold Loan, the interest structure is clearly communicated upfront. Borrowers are informed about:

- The annual interest rate

- Processing charges (if any)

- Tenure options

- Repayment flexibility (EMI, bullet repayment, or part-payments)

The terms and conditions are duly documented in Key Facts Statement. The borrower receives a formal loan agreement and repayment schedule, ensuring there are no surprises later.

In contrast, traditional pawnbrokers often operate with less transparency. Interest may be quoted monthly without clearly stating the annualised rate. Additional penalties, compounding structures, or late fees may not be fully explained at the outset. What initially seems like a small percentage can become significantly expensive over time.

With organised gold loans, clarity reduces financial stress. With informal pawning, ambiguity can increase it.

- Security of Pledged Gold: Structured Safeguards vs. Informal Storage

When you pledge your gold, safety is paramount. After all, these are often family heirlooms or assets of deep emotional value.

Regulated gold loan providers maintain:

- Secure vault storage

- CCTV-monitored premises

- Insurance coverage for pledged gold

- Tamper-proof packaging and documentation

Gold is catalogued, sealed, and stored in professionally managed vaults. The borrower receives proper documentation confirming weight, purity, and pledged items.

On the other hand, unregistered pawnbrokers may store gold in less secure environments. Insurance coverage may not be guaranteed. Documentation may be limited to a simple receipt, without detailed breakdowns.

In the unfortunate event of loss, theft, or dispute, recovery mechanisms in informal settings can be complicated and uncertain.

With an organised lender, systems are built around accountability and protection.

- Regulatory Protections: RBI-Governed vs. Unregulated

Organised gold loan providers operate under the regulatory framework of the Reserve Bank of India (RBI) when structured as NBFCs or banks. This brings multiple borrower safeguards, including:

- Defined Loan-to-Value (LTV) caps

- Transparent auction procedures (if repayment defaults)

- Fair practices code

- Customer grievance redressal systems

- Clearly documented terms and conditions

If a borrower faces a dispute, there are official escalation mechanisms available.

Unregistered pawnbrokers, however, may not operate under the same regulatory scrutiny. Terms may vary widely from one operator to another. In cases of disagreement regarding interest, valuation, or auctioning of gold, borrowers may have limited legal recourse.

Regulation is not just paperwork it’s protection.

- Valuation Transparency: Scientific Assessment vs. Subjective Pricing

The amount you receive against your gold depends on accurate valuation.

Organised lenders use:

- Standardised purity testing methods

- Calibrated weighing systems

- Transparent loan-to-value calculations linked to prevailing gold prices

You are informed about:

- The assessed purity (karat level)

- Net weight considered (after excluding stones)

- Current gold rate applied

- Maximum eligible loan amount

This clarity ensures you understand exactly how your loan amount is derived.

In contrast, informal pawnbrokers may use subjective evaluation methods. The gold rate applied may not always match prevailing market rates. Purity deductions or weight adjustments may not be fully explained.

Even small discrepancies in valuation can significantly reduce the loan amount offered. Transparency ensures you unlock the true value of your gold.

- Potential Risks of Unregistered Pawnbrokers

While pawning may appear convenient due to proximity or familiarity, it carries potential risks that borrowers should carefully consider:

- a) High Effective Interest Costs

Monthly interest may appear small but can translate into very high annual rates. - b) Compounding Without Clear Disclosure

Interest-on-interest calculations may not be fully explained. - c) Short Repayment Windows

Failure to repay within tight timelines could lead to quick disposal of pledged gold. - d) Limited Documentation

Minimal paperwork can create challenges in case of disputes. - e) Auction Without Standardised Process

In case of default, gold may be sold without structured communication or transparent valuation.

When financial pressure is already high, these risks can add further strain.

The Emotional Aspect: It’s More Than Just Gold

For many families, pledged gold represents memories wedding jewellery, inherited ornaments, milestone gifts. Losing it due to unclear loan terms or avoidable miscalculations can have emotional consequences far beyond monetary value.

Choosing a structured, regulated gold loan ensures that even during financial urgency, your asset remains protected within a system designed for fairness and accountability.

Why Organised Gold Loans Are the Safer Choice

When comparing gold loans and pawning, the distinction becomes clear:

| Factor | Organised Gold Loan | Informal Pawning |

| Interest | Transparent & documented | Often unclear or monthly-based |

| Gold Storage | Insured & secured vaults | May lack structured security |

| Regulation | RBI/NBFC governed | Often unregulated |

| Valuation | Standardised testing | Subjective assessment |

| Dispute Resolution | Formal mechanisms available | Limited recourse |

While both options provide immediate liquidity, only one combines speed with structured protection.

Making an Informed Decision

Financial urgency can sometimes push borrowers toward the quickest visible option. But taking a few minutes to understand how your loan works can prevent months of financial stress later.

Organised gold loans offer:

- Quick processing

- Minimal documentation

- Transparent pricing

- Secure storage

- Flexible repayment options

Most importantly, they provide peace of mind. When pledging something as valuable as gold, clarity, safety, and fairness should never be compromised.

Before making your next borrowing decision, ask yourself:

Are you simply pawning your gold or are you choosing a structured financial solution designed to protect it?

The difference could be far more valuable than the loan amount itself.