The has been a sharp increase in the gold loan demand. As per RBI reports, the loans against gold during 2025 almost doubled. More and more people are turning to gold loans because they are quickest and hassle-free means of financing. With such increasing popularity of gold loans, it is important to know and avoid the most common mistakes borrowers end up doing.

Uncertainties prevail, be it with the job, business or even the stock market. However, the aspirations and dreams keep driving. And to fulfil these dreams gold loans are the best as they allow the borrower to leverage your idle gold jewellery and coins to get access to funds quickly. A new gold loan borrower can easily make a mistake while applying gold loan. And one wrong step can lead to delays in approval, lower loan eligibility or even loss of precious gold! In this blog we share the common loan application errors and guide you to avoid mistakes while availing a gold loan.

Due diligence and KFS is Must

The borrower must be extra careful with gold loan applications. He must exercise complete diligence while applying for a gold loan. What is done in a hurry often lands in worry. Signing the gold loan agreement in a rush can mean reduced loan amounts, higher rate of interest, or even a loss of pledged gold. Before finalizing the gold loan provider, a thorough research and comparative study on providers, loan amounts, tenure, rates, and potential pitfalls should be done. The borrower having information on competitive loan providers is always better placed to negotiate on interest rate and maximise the eligibility of the gold loan.

The Must Do Acts While availing the Gold Loan

The borrower must do the below while availing the gold loan:

Check Gold Purity

The loan amount always depends upon on the purity of the gold pledged. The lenders provide gold loans against jewellery of 18K to 24K purity. Any stones, gems or other metal is deducted before valuing the gold. The borrower gets the loan only against the actual gold content.

The borrower must check the hallmark and verify the purity of the gold that is intended to be pledged.

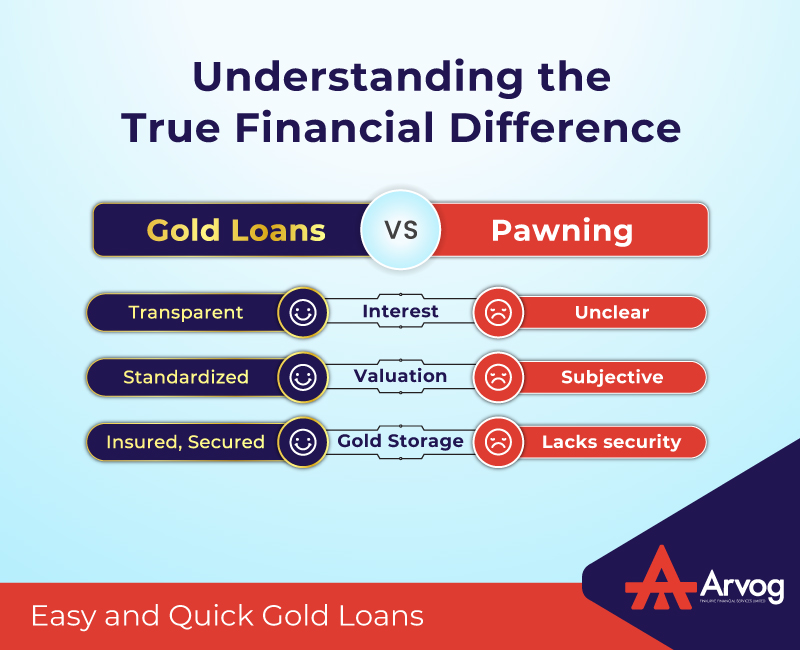

Due Diligence Check and Research

The lenders trustworthiness is most important in case of gold loans. As the borrower pledges the valuable gold as collateral. To have a total peace of and assurance for the security of the asset is secure.

There are risks like:

- Loss of gold if the lender shuts operations

- Delayed retrieval of pledged security after loan closure

- Charges that were not shared beforehand are levied

As an informed borrower one must ask for and check:

- Registered business with RBI approval

- Security protocols for storing pledged gold

- All charges and costs including processing fees

- Complete retrieval process for pledged gold

Competitiveness

When choosing between different lenders like, banks and NBFCs for the gold loan, it is important to compare their rate of interest and other parameters. One key factor is gold valuation, typically NBFCs provide higher loan amounts against pledged gold than banks due to more flexible LTV policies.

The borrower must analyse the key parameters like gold valuation, interest rates, processing fees and application process of all probable lenders for the gold loan before finalising the best suited loan provider.

Check Repayment Terms

Always check the repayment plans that the lender offers, like:

- Bullet repayment: Interest-only payouts during tenure, principal at maturity

- EMI: Fixed monthly payouts covering interest and principal

- Part-prepayments: Option for partial principal payouts during tenure

The borrower must choose the option that best fits his cash flows. A mismatch between repayment capacity and repayment structure can risk loan default.

Evaluate Loan Tenure

Generally, the gold loans allow tenures ranging from 6 months to 24 months (2 years). An unrealistic tenure will hamper repayment discipline. The borrower must consider below for the loan tenure:

- Purpose of loan- Shorter tenure for emergency funds, longer for business needs

- Income stability – Salaried prefer shorter, self-employed longer tenure

- Interest cost – Longer tenure means higher interest outgo

Comparing Interest Rates

The borrower must compare the interest rates on gold loans from banks as well as NBFCs.

Don’t Fall for Wrong Promises

Some lenders make tall claims, for example ‘Zero interest for 30 days” on gold loans. The interest in such cases is charged but hidden in the processing fee. Or the claim mentioning ‘Instant gold retrieval”. There is always a processing time and sometimes cost too involved for the retrieval of gold pledged. The borrower must read the terms & conditions and avoid misleading claims. The genuine lender will always mention upfront the realistic turnaround times and the costs involved.

Conclusion

The borrower can avoid the errors by being aware via KFS and competitive analysis while applying for a gold loan.