Introduction

Gold’s allure and dominance as the principal medium of trade have captivated all civilizations around the world since the beginning of time. Because of its inherent excellence, pristine condition, potency, and demand, it has always stood as a symbol of its owners’ pride.

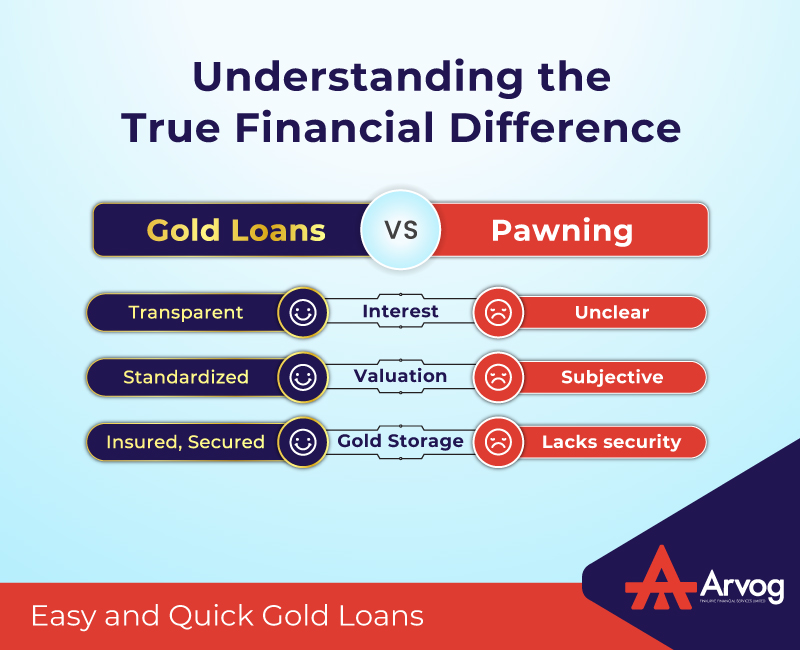

The rising value of gold means that you can now borrow more money against it. By using your jewellery as collateral for a loan, you’ll be able to take advantage of more favorable interest rates from more lending institutions.

A Gold Loan might be a lifesaver for consumers who believe they have exhausted all other choices for meeting their financial necessities. The gold loan market is a $6 trillion sector, with banks and Non-banking Financial Corporations splitting the revenue 80:20 respectively.

However, there are nuances to a Gold Loan that not everyone is aware of.

Now, let’s take a look at the exclusive features of a gold loan.

1. Swift Loan Disbursal :-

Gold loans are widely used in India because of their convenience and speedy funding. The value of gold jewellery, coins, and bars may be used as collateral for loans when pledging these items to a lender.

The RBI guidelines on gold by banks state the loan amount is anywhere around 75% of the value of the gold that was pledged. Because gold loans are collateralized, lenders may quickly approve them without conducting comprehensive background checks or needing proof of income or employment.

2. Lenient Credit Evaluation

Gold loans are collateralized loans since the borrower pledges tangible gold as security. In the event of default, the gold pledged as collateral will be sold and the proceeds returned to the lenders. This means that the borrower’s credit score isn’t as important, making gold loans available to those who otherwise wouldn’t qualify. In addition, regular repayments may help borrowers improve their credit scores. As a result, the client benefits on both ends of the transaction.

3. Favorable Interest Rates

The low interest rates offered by gold loans make them a popular alternative to high-interest personal loans and credit cards. Even if the borrower fails on the loan, the lender may rest easy knowing they will get their gold back. Since the lender is taking on less risk, they may afford to provide more liberal interest rates.

The value of the gold pledged is used to calculate the maximum loan amount available to the borrower, known as the loan-to-value (LTV) ratio. In certain cases, interest rates might be reduced even more by decreasing the LTV ratio.

4. Customizable Loan Repayment

It’s possible that no other loan offers as many flexible repayment options as a Gold Loan. There are several options for paying back a gold loan from which one can choose. You may choose a repayment schedule that works best with your budget and lifestyle needs.

The principle and interest on certain gold loan schemes may be repaid in one single “bullet payment” after the loan’s term. Partially repaying a gold loan is also possible at any time throughout the loan’s term. With this flexibility, borrowers may make payments less often as needed, successfully managing their finances.

5. Multiple Loan Opportunities

There is no limit on how many times you may take out a loan against your gold. Simply pay off the current debt and choose a Gold Loan at your convenience. Remember, you can get a Gold Loan for the same accessories or coins as many times as you wish, but not simultaneously. Pay down the initial gold debt and lenders will then give you back whatever gold you borrowed.

Taking out a gold loan has several advantages and may save you from financial disaster. When compared to other loan choices, gold loans in India have the advantages of quick disbursal, low documentation, and streamlined paperwork. However, before committing to a gold loan, it is always wise to do your homework.

Who we are:-

Arvog is a new-age, AI/ML-powered, customer-centric finance company that makes digital lending quick, efficient, and easy. We focus on digital personal loans and digital gold loans.

{kind=link}